Pet Care Insurance Statistics: 2025 Lookback Report

Pets are unpredictable. It’s part of their charm. But the quirks that delight and frustrate pet owners can escalate into expensive claims for pet care professionals.

This report summarizes real Pet Care Insurance (PCI) liability claims with 2025 dates of loss and pairs them with PCI survey insights. Together, these pet care insurance statistics reveal the true impact of pet-related accidents, as well as the role of pet business insurance in trust and risk management for pet services.

Key Pet Care Business Insurance Statistics & Findings

Information sourced from 2025 PCI internal claims data and PCI’s 2024-2025 Behind the Leash pet business trend report

Standout Stats from the Collected Data:

- The median claim cost for pet professionals is $1,266, meaning even routine accidents can carry real weight for pet professionals.

- The most expensive 3.1% of claims accounted for 24.3% of total costs, showing that rare, high-severity claims drive a disproportionate share of pet care losses.

- The largest 2025 claim reached $94,375 with a chain reaction of pet injury, human injury, and legal costs.

- 65.6% of claims involve pet injury, illness, or death while in care, making it the core liability exposure for pet pros.

- Low-frequency claim types like third-party bodily injury (just 2.4% of total claims) account for an outsized share of total costs (10.1%).

- 80% of pet owners are more likely to hire insured pet pros, positioning insurance as both protection and a trust signal.

2025 Pet Care Liability Claim Cost Statistics

The average cost of a pet care liability claim only tells part of the story. A small number of high-cost incidents pull the average up, while the median shows what most pet professionals actually experience.

In 2025:

- Claims analyzed: 636

- Total incurred: $1,484,669.67

- Median (typical) claim: $1,286.75

- Mean (average) claim: $2,345.45

- Range: $90 to $94,375

The gap between median and average matters for pet pros. The median represents a typical claim, while the higher average is driven by less frequent, high-severity losses.

Claim distribution shows how these costs stack up:

- 25th percentile: $687.75

- 75th percentile: $2,498.80

- 90th percentile: $4,718.05

- 95th percentile: $7,377.87

Most claims fall within a manageable range, but costs rise quickly as incidents become more complex. This illustrates why insurance is crucial in pet care for low-frequency, high-impact accidents.

Only:

- 3.1% of claims exceeded $10,000, accounting for 24.3% of total costs

- 0.3% exceeded $20,000, accounting for 8.2% of total costs

- 0.2% exceeded $50,000, accounting for 6.4% of total costs

For many pet care businesses, even a “typical” claim is significant. Nearly half (49.7%) of pet professionals reported earning $34,999 or less annually from pet care, meaning a four-figure loss would be a meaningful share of their income. A high-severity claim could exceed what many part-time or gig-focused pet professionals earn in a year.

Note: Claim costs represent total incurred amounts, including indemnity, administrative and processing expenses, and defense costs.

Takeaway: Most pet care claims are manageable, but not minor. A typical claim costs just over $1,200, while a small number of high-severity outliers drive a disproportionate share of losses. This can quickly turn routine work into a serious financial risk without the right coverage.

Our Largest Pet Care Claim: Pet Risks and the Snowball Effect

PCI’s highest 2025 claim explains how an everyday walk can spark a chain reaction of liability costs, creating rare but expensive and complex claims for pet professionals.

Largest incurred pet care claim: $94,375

In this case, a dog walker took a dog out for a walk on a public sidewalk. Nearby construction disrupted the flow of foot traffic, bringing the dog into close contact with other pets and people. The dog became nervous. At the worst possible moment, a metal component of the leash failed, allowing the dog to break free.

The loose dog attacked another dog, resulting in bite injuries that needed emergency treatment. As the other dog’s owner tried to intervene, they suffered a knee fracture, ligament damage, and multiple lacerations, including a significant hand injury.

The incident escalated into a lawsuit, naming the dog walker as the dog’s “keeper” under a state liability statute, along with the dog’s owner. This is often how routine pet care turns into multi-layered claims involving pet injury, human injury, and legal action. It is also why the cost-to-benefit of pet care insurance can be so high for pet professionals.

Takeaway: The most expensive pet care claims rarely have a single cause. They’re a combination of factors, like pet injury, human injury, and legal exposure. Even basic care, like walking a dog, can carry real risk when an unpredictable environment or equipment failure triggers a liability chain reaction.

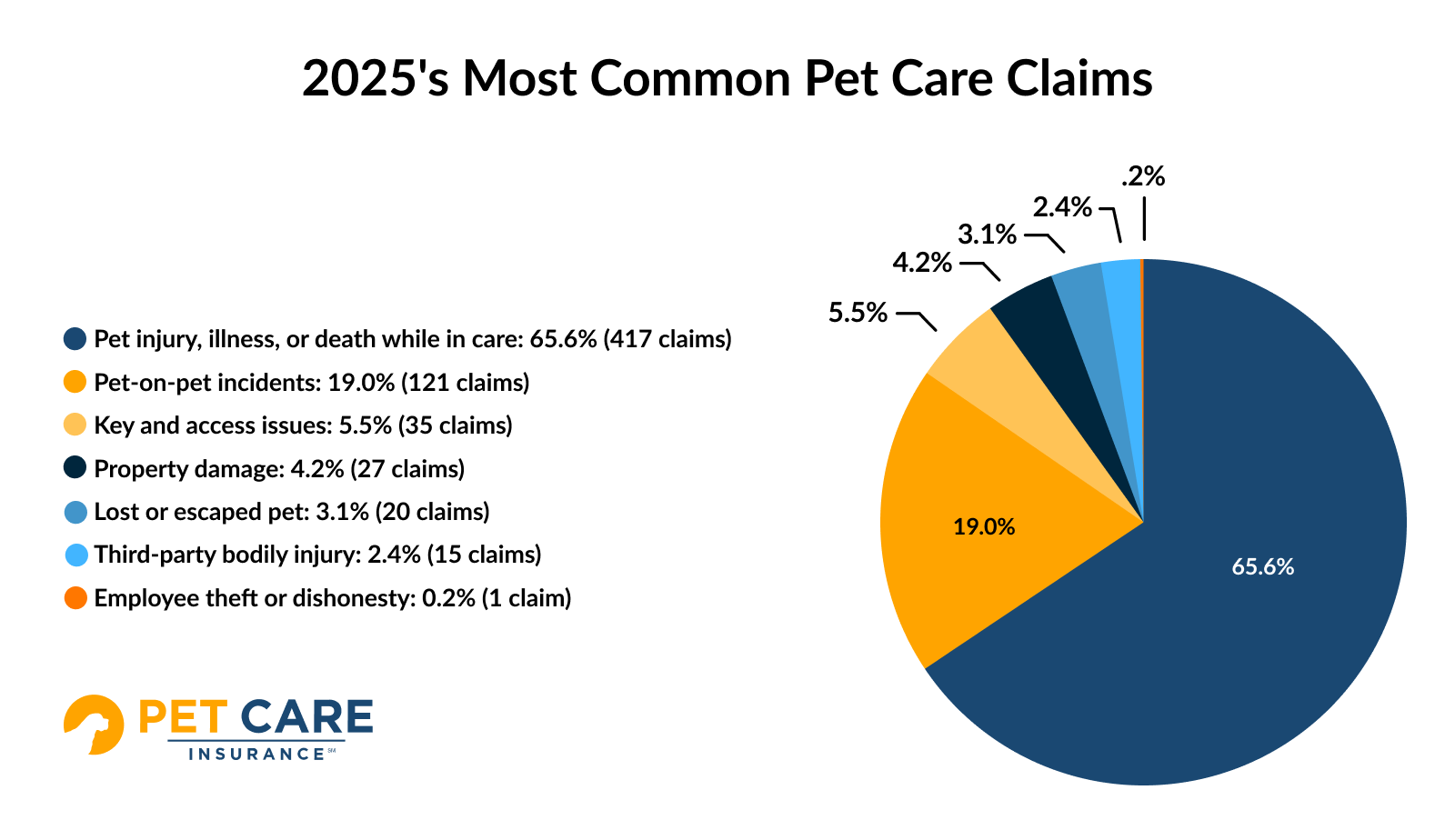

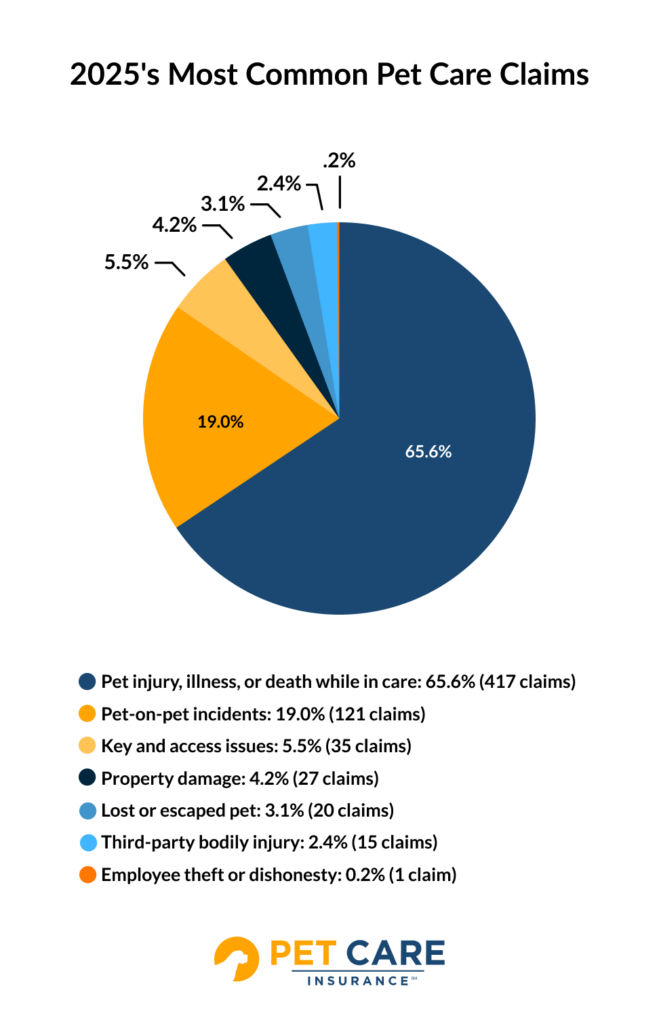

Most Common Pet Care Insurance Claims

Most pet care claims fall into a small number of recurring scenarios tied to everyday work.

The standout observation is how concentrated a pet caregiver’s risk really is. Nearly two-thirds of claims involve a pet getting hurt, sick, or worse during care. The next most common issues, like pet-on-pet incidents and access problems, reflect the realities of handling animals, managing environments, and working in clients’ homes.

Common loss scenarios for harm to pets and pet-on-pet injury claims:

- Pets ingest foreign objects or are physically injured during normal supervision

- Triggers like food, toys, or rough play lead to fights in multi-care settings

- Encounters with unfamiliar dogs during walks escalate into injuries

Less frequent claims, like third-party injuries or lost pets, tend to be more complex. They can involve medical bills, legal action, or additional expenses like search efforts and recovery costs.

Other common loss scenarios include:

- Lockout, lost key, or lock/code issues requiring locksmith services

- A dog slips a harness or escapes during transport or handoff, later requiring veterinary care

- A cat escapes the client’s home and goes missing during care

Takeaway: Most pet care claims aren’t edge cases. They’re tied to routine responsibilities like supervision, managing multiple pets, and gaining access to clients’ homes. The same tasks pet professionals perform every day are the ones most likely to lead to a claim if something goes wrong.

Pet Injury Claims Are the Biggest Risk in Pet Care

Pet injury claims are a pet professional’s single greatest risk, making up 65.6% of all claims in 2025.

These incidents follow some clear patterns:

- Physical injuries and trauma: 38.1% of pet-harm claims

- Grooming-related injuries and reactions: 23% of pet-harm claims

- Ingestion of a toxin or foreign object: 18.2% of pet-harm claims

- Sudden-onset illness or collapse: 12.5% of pet-harm claims

- Pet death: 8.2% of pet-harm claims

In other words, the most common claim in pet care is also the one most likely to happen during everyday work. Most of these incidents occur during routine care, such as grooming, feeding, or exercise. However, the most severe outcomes carry disproportionate cost. Pet death accounts for just 8.2% of pet-harm claims, but 18.3% of total costs.

Coverage for the biggest risk in pet care is also one of the industry’s most common coverage gaps. Standard general liability policies often exclude animals in your care, custody, or control, meaning many pet professionals may not be covered for their most likely claim.

Pet care-specific insurance addresses this through Animal Bailee coverage, which can help protect against the costs of injuries, illness, loss, or death of a pet under a pet pro’s supervision.

Takeaway: The biggest risk in pet care is the work itself. Common tasks like grooming, feeding, and handling are where most claims happen, but good prevention habits reduce the likelihood of accidents.

Proper pet business insurance is also part of managing routine risks. Animal bailee, pet protection, or care, custody, and control coverage can help pet professionals address their most common claims.

Human Injury Claims Aren’t Just Bites: A Surprising Pet Care Insurance Statistic

Bites are usually the first thing that comes to mind for pet liability. Most human injury claims in pet care do involve bites, but they’re not what drives the highest costs.

- Bite, nip, and scratch incidents accounted for 73.3% of human injury claims

- Falls, knock-downs, and intervention-related injuries made up just 26.7% of claims, but 66.7% of total costs

In 2025, claims included an elderly person falling backward after an interaction with a dog in an elevator, leash tangles resulting in lost balance, and multiple people harmed while stepping in to break up animals fighting. Incidents during interactions with neighbors and their pets or other dogs outside the home are common.

These situations tend to lead to more serious injuries and complications that increase medical costs and legal exposure.

Takeaway: Bites are the most common human injury risk, but not the most expensive. Falls and intervention-related injuries drive the highest costs. Handling protocols, controlled interactions, and strong leash practices can reduce these incidents, especially in unpredictable environments.

Which Pet Services Show Up Most in Claims

Not all pet care services carry the same level of risk. The services with the most claims aren’t always the ones with the most providers.

In cases where pet service type was clearly identified, 2025 claims were distributed as follows:

- Grooming: 34.0% of total claims

- Walking or waste removal: 20.8% of total claims

- Daycare or boarding: 20.0% of total claims

- Sitting or drop-ins: 13.2% of total claims

- Training: 7.5% of total claims

- Taxi or Transport: 4.5% of total claims

Compared to the percentage of policyholders in each category, some services drive an outsized number of claims. This suggests a riskier service. PCI’s policyholder mix includes:

- Walking or waste removal: 31.9% of policyholders

- Sitting or drop-ins: 28.8% of policyholders

- Daycare or boarding: 9.4% of policyholders

- Taxi or transport: 8.2% of policyholders

- Grooming: 7.9% of policyholders

- Training: 7.6% of policyholders

- Other: 6.2% of policyholders

For example, grooming makes up just 7.9% of PCI policyholders, but 34% of overall claims, suggesting a higher concentration of risk. On the other hand, pet sitting represents 28.8% of policyholders but only 13.2% of claims, indicating a lower relative claim frequency.

Takeaway: Some pet care services carry more inherent risk than others. Higher-contact, higher-control environments, like grooming, walking, and group care, tend to generate more claims. Understanding where services fall on that spectrum can help pet professionals and insurers prioritize both prevention and the proper level of coverage.

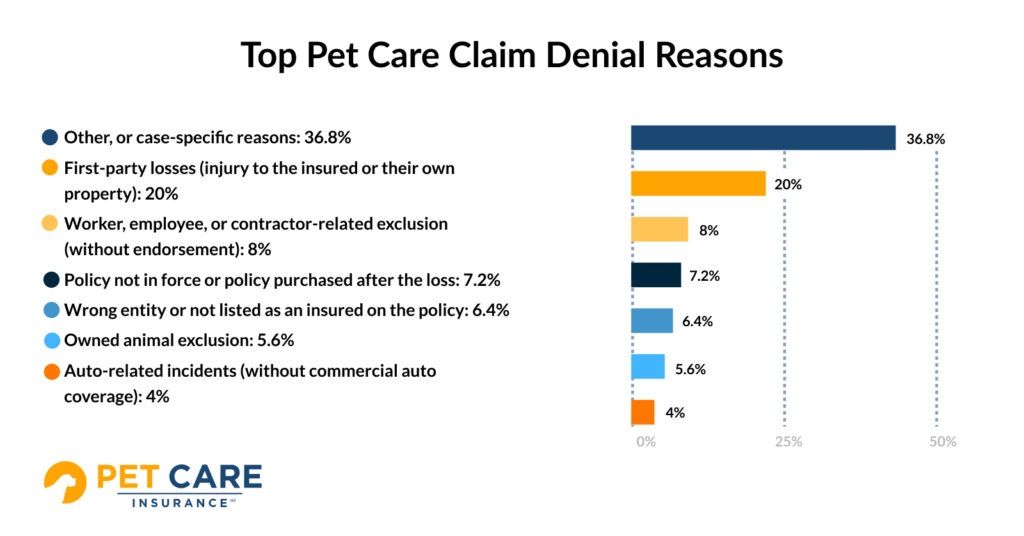

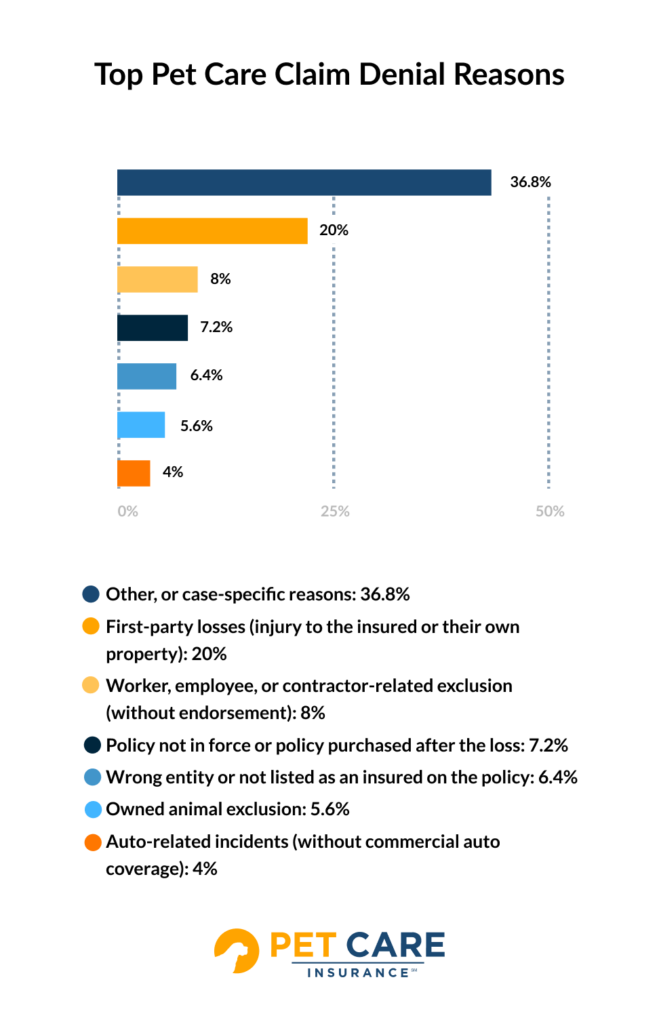

Why Pet Care Liability Claims Get Denied

Claim denials are not random, although they can feel that way to pet professionals. Denied claims usually come down to a mismatch between what happened and what the policy covers.

Based on 125 denied claims from 2025, the most common causes were:

Note: Claims in remaining categories (not pictured) represented 3% or less of total denied claims.

Most of these denials come down to clarity around who is covered, when, and under what circumstances. Pet care pros can avoid many claim denial issues using a few upfront checks:

- Match your policy to your services. For example, if you transport pets for work, Commercial Auto Insurance could cover those risks.

- Understand first-party vs third-party claims. Liability coverage usually applies when the harm is to others or their pets (third-party), not to you, your employees, or pets you own (first-party).

- Keep coverage active before taking clients. You typically must be insured when the incident occurs to be covered.

- Confirm that your business details are correct. Your business name, details, and Additional Insureds need to be correctly listed and up-to-date on your policy.

Takeaway: Most denied claims in pet care are preventable. When coverage matches the work and is active at the right time, pet pros are far less likely to run into issues with their insurance if something goes wrong.

Insurance Is a Trust Signal in Pet Care

Insurance is part of most pet owners’ hiring decisions, whether it is discussed or not.

According to PCI’s 2024-2025 survey of pet owners:

- 80% of pet owners are more likely to hire a pet professional with insurance

- 29% of pet owners say they actively ask if a pet pro is insured

- 74% of pet professionals say clients value their insurance

- 80% of pet professionals say they communicate or advertise that they’re insured

Most pet care clients won’t ask about insurance directly because it is often assumed. This means promoting coverage reinforces a pet owner’s trust and expectations, but not having insurance can be a serious issue for pet pros.

The kind of insurance also matters in pet care. Some pet pros assume the growing popularity of pet health insurance among pet owners means their work is covered. However, pet health insurance covers the animal’s medical care, not a pet professional’s liability. That responsibility falls back on the caregiver’s business.

This makes business insurance visibility and coverage crucial. Simple signals, like providing a COI, adding a note to booking confirmations, or displaying an insurance badge, can build trust before a client even thinks to ask.

Takeaway: Pet care insurance protects more than a pet professional’s business. It helps win work. Even though pet owners rarely ask about coverage directly, the majority say it directs their decisions about who to book. Showing coverage influences how they evaluate trust and professionalism.

Practical Ways to Reduce Pet Care Liability Claims

Most risks in pet care are predictable, which means many claims are also preventable. When paired with insurance coverage designed for pet care, a few simple systems can help protect pets and businesses. Pet pros can take steps like the following to reduce their liability:

- Standardize intake with clear notes on diet, behavior, and emergency contacts

- Set care and emergency protocols, including vet authorization

- Control pet introductions and high-risk triggers in group settings

- Track keys and access with consistent processes and backup contacts

- Pet-proof environments and follow client house rules

- Check equipment regularly and use safe handling practices during walks

Additional resources:

Methodology

This report combined Pet Care Insurance (PCI) statistics from 2025 internal claims data with a nationwide survey of pet owners and pet professionals conducted from 2024-2025.

Claims Report Data Methodology

- Sourced from internal PCI pet care liability insurance claims and loss data with loss dates from 2025

- Claims that match PCI’s covered pet care operations and third-party liability claims were included in this report

- Calculations refer to the total incurred cost for all loss instances, including indemnity, defense, and expenses, and may include estimates for open claims

- Claims were grouped into categories to highlight trends in real loss narratives

Pet Ownership and Pet Services Survey Methodology

- Surveys were conducted between August 2024 and January 2025

- Three internal surveys polled PCI-insured pet care providers (conducted by PCI)

- Survey 1 sample size: 546 U.S. adults

- Survey 2 sample size: 47 U.S. adults

- Survey 3 sample size: 166 U.S. adults

- One external survey polled pet owners (conducted by Virgo PR for PCI)

- Sample size: 491 U.S. adults

- Results were published in Behind the Leash: Insights From Pet Professionals, Pet Parents, and Industry Statistics

- Survey results were contextualized using policyholder database analysis of 15,460 PCI-insured pet professionals